Theme impact

The impact of IoT on the financial services industry

Credit: Bert van Dijk/Getty images.

Powered by

Interactions between customers and connected devices yield two primary business avenues for financial services companies. The first, and most apparent, is the ability to embed products and services into user interfaces and applications, ultimately boosting revenue. The second is the treasure trove of customer insights that can be extracted from user-generated data and the subsequent opportunities for more nuanced personalisation. Historically, banking and payment companies have predominantly focused on the former, while insurance companies have leaned into both.

While there is scope for incumbent financial services companies to sell proprietary IoT devices like mobile point-of-sale (mPoS) systems or telematics equipment for cars, the majority of IoT integration across the sector occurs via third-party consumer electronics devices like mobile phones, laptops, and smartwatches.

This places a greater emphasis on software as opposed to hardware, for which the natural prowess lies with Big Tech players like Google, Apple, and Samsung Electronics. Some companies have had more ambitious visions in this respect. Mastercard and Visa, for example, both share the vision of making all connected devices payment-enabled.

However, more ‘things’ connected to the internet have blurred the product and provider boundaries further, empowering Big Tech players while relegating incumbents to more functional or modular plays. Furthermore, IoT devices create more data points for financial services companies to capture, which may not have been explicitly permissioned by users and customers. IoT also leads to more endpoints for potential cyberattacks, exacerbating what is already a widespread issue for the sector.

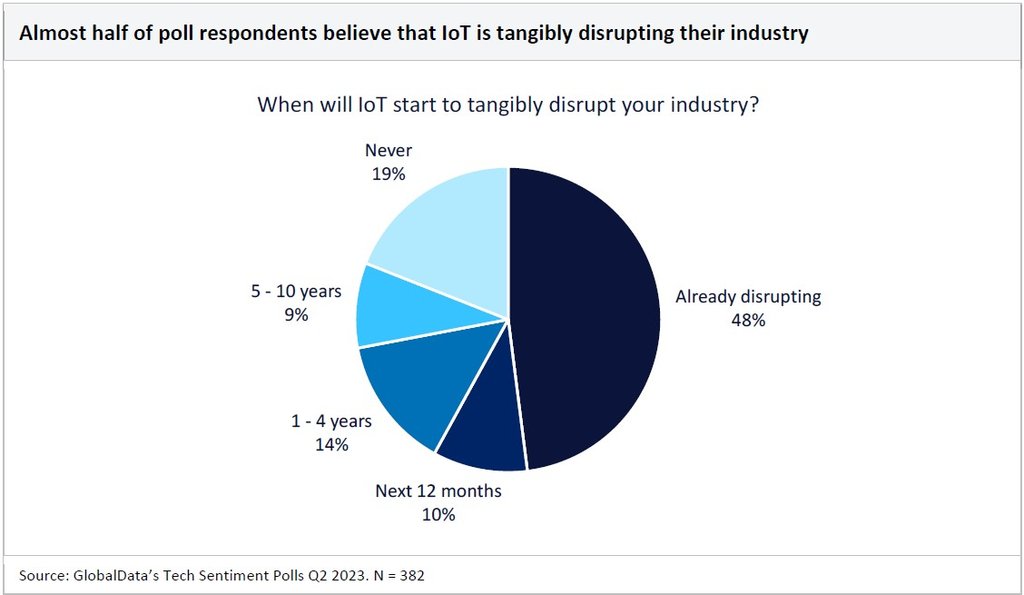

IoT is already disrupting the financial services landscape, so most use cases across the sector have been explored. Combining IoT with other technologies has created opportunities for further innovation. For example, some banking and payments companies, such as JPMorgan Chase, JCB, and Mastercard, have explored the interplay between IoT in blockchain.

In addition, the growing sophistication of generative AI could prove crucial for effectively conveying insights from IoT devices in natural language to customers and clients. Increasing tech regulation will place continued pressure on financial services companies in this regard to provide transparency into how customer data is being used.

Impact assessment and investment opportunities

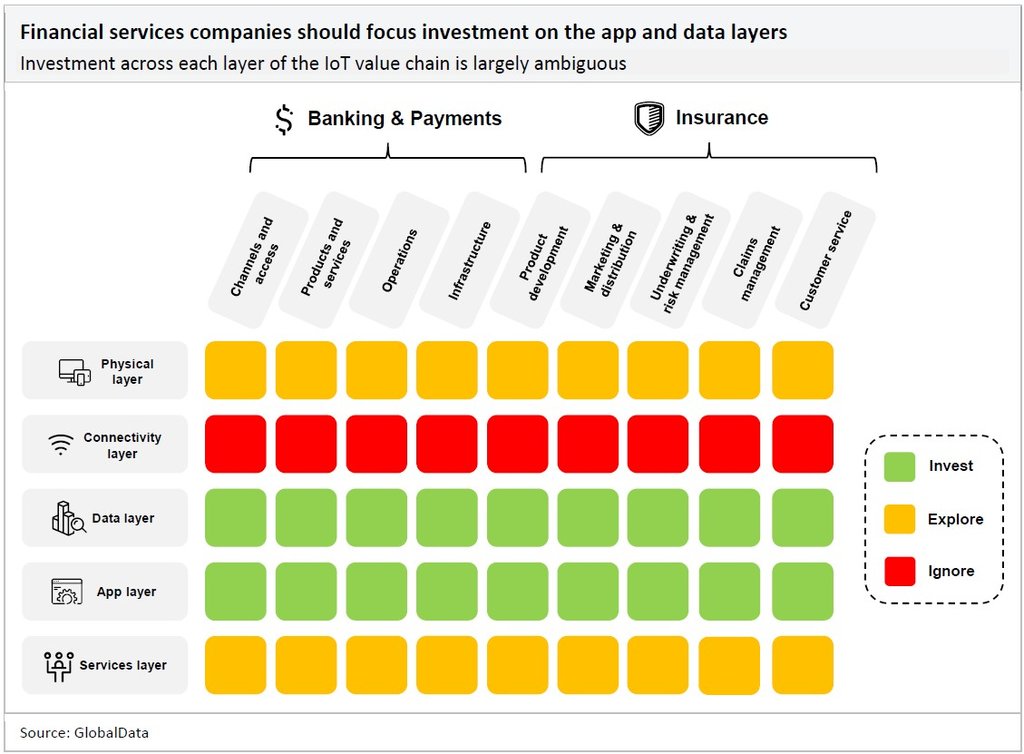

The matrix below details the areas in IoT where companies operating in the financial services sector should focus their time and resources. We suggest that financial institutions invest in technologies shaded in green, explore the prospect of investing in technologies shaded in yellow, and ignore areas shaded in red.

Investment across each layer of the IoT value chain is largely unanimous for the financial services sector. In the physical layer, companies can explore the development of point-of-sale (POS) terminals to accept payments, dedicated devices like rings and key fobs to deliver payments, or wearables to track health metrics.

However, in most cases, the adoption of IoT occurs through third-party device manufacturers and tech companies that allow financial services companies to embed platforms and payment gateways into their user interfaces. In this respect, investment in the app layer will be key to ensuring companies maintain a presence across these devices.

Investment in the connectivity layer can be ignored as proprietary networks for IoT devices would be unnecessarily costly and complex to develop in-house. In this respect, financial services companies will encounter the ‘cold start problem’ that hinders the progress of public goods like wireless networks, as there is a reluctance among participants to take unilateral risks without incentives, especially when more widely adopted and functional networks already exist.

The financial services sector holds a plethora of user data and customer information. Sensors will generate even more data as IoT grows and develops. In some instances, the sheer volume of data collected at the edge of the network makes it unfeasible to transport it to a central hub, so it must be processed at the edge. Investment in the data layer is therefore crucial to ensure that customer insights are processed seamlessly.

Financial services companies can explore the prospect of providing IoT-related services. However, they may find it difficult to compete with IT and professional services companies that have built up specialist teams dedicated to providing IoT-related services. Therefore, the best route to market for this will be working with small-to-medium enterprises (SMEs). For example, HSB is an insurtech that offers a full suite of commercial, industrial, and residential IoT solutions for SMEs.

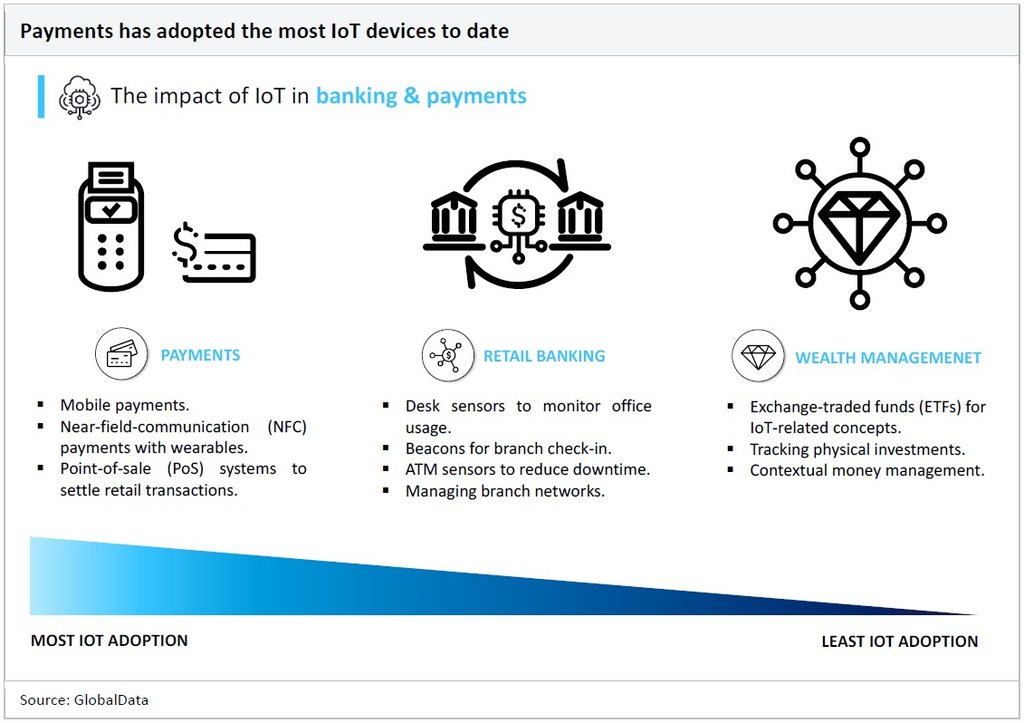

The impact of IoT in banking & payments

IoT in banking was often viewed cynically as a vendor construct that was pushed onto the industry, as the use cases were always more compelling for other verticals that had more ‘things’ to connect, notably the insurance industry which has integrated the technology across almost all products and offerings. Payments has naturally adopted the most IoT devices, followed by retail banking and wealth management.

IoT has historically been one of the least used technologies in branch transformation but has some applications that retail banks have explored. Notably, beacons, which are small Bluetooth-based transmitters that connect with smart devices nearby, have allowed branches to personalise their customer services and gain instant feedback from their clients. When a customer walks into a branch, banks can decide who should serve them based on their profile and needs.

Beacon technology also alerts employees to customers with disabilities so that they can provide them with the needed support. Other than that, customers can immediately give their feedback once they exit the branch which allows banks to improve their overall services.

Citibank boasts perhaps the most advanced beacon deployment where customers can unlock doors through mobile apps, and receive relevant notifications regarding offers or services, queue time guidance, and the option to participate in surveys. Citi mines data from beacons to help manage queue times and decide when to add more tellers.

BMO Harris Bank in Canada tested something similar, in which branch locations have no humans present ‘front of house’, and customers are instead guided by chatbots and connected devices. If the system malfunctions, customers are transitioned to a video conference option.

The continued use of beacon technology by banks depends on how well they are adopted. Westpac was an early adopter of beacon technology in-branch but decided not to adopt the technology on a wider scale after running trials in New Zealand. The future of beacon technology also hinges on the future of branches, which is a heavily debated topic.

Other applications include the use of IoT to monitor ATM performance. For example, DBS partnered with A*STAR to install sensors in its ATMs that detect abnormalities, use AI to identify patterns, and reduce downtime for customers. In 2017, some retail banks experimented with sensors that sit underneath office workers’ desks to track activity and desk usage. Examples include Société Générale, Deutsche Bank, Lloyds Banking, and Barclays.

As expected, the deployment of this technology was an unpopular decision and was soon reversed. While many banks like Barclays claimed that the technology was being used to monitor productivity and assess office space, most workers felt as if their privacy was being violated.

GlobalData, the leading provider of industry intelligence, provided the underlying data, research, and analysis used to produce this article.

GlobalData’s Thematic Intelligence uses proprietary data, research, and analysis to provide a forward-looking perspective on the key themes that will shape the future of the world’s largest industries and the organisations within them.