Theme impact

Net-zero strategies for the financial services sector

Credit: Bert van Dijk/Getty images.

Powered by

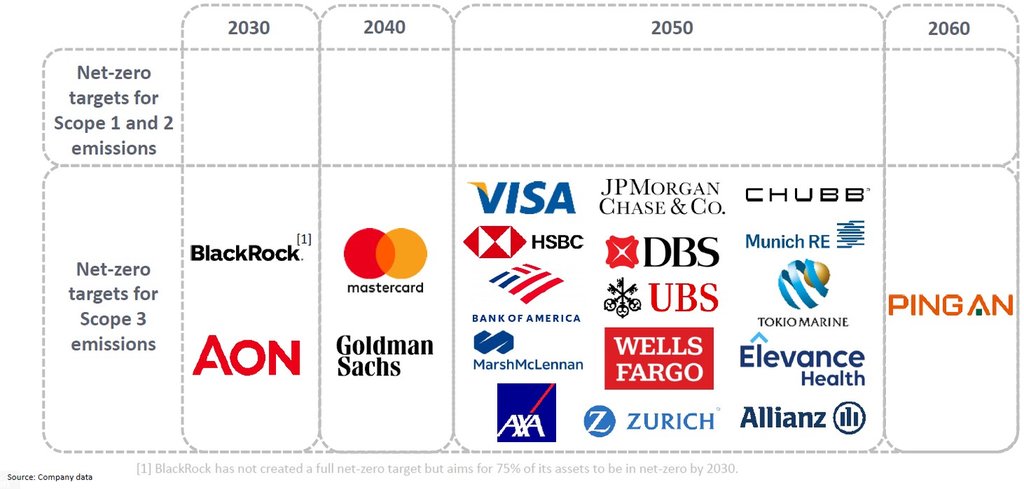

Financial services are facing new challenges in achieving net zero by 2050. All 20 of the leading financial services companies analyzed by GlobalData have committed to achieving net zero emissions across select areas of their value chains between 2030 and 2060.

Scope 1 and 2 emissions, which are generated by business operations, make up 29% of currently reported emissions. Efforts to reduce Scope 1 and 2 emissions include carrying out green renovations on corporate offices and data centers, purchasing renewable energy, and using sustainable aviation fuel for company-owned jets. Scope 3 emissions, or value chain emissions, account for 71% of emissions but are currently under-reported. The main contributors to upstream Scope 3 are purchased goods and services and business travel.

In the next five years, financial services companies will need to focus on financed emissions. These emissions are those linked to the financial services companies’ assets and liabilities. This category is emerging, so while some companies have started setting targets to reduce financed emissions associated with key sectors in their portfolios, reporting is still sparse. Finance majors will need to report on these emissions more comprehensively.

Financial services companies are creating climate-focused investment products, but these bring greenwashing risks. This includes debt and equity investments and corporate banking and insurance services. The most common among these is green bonds. To avoid scrutiny, finance majors should carry out robust auditing of ESG-focused offerings and ensure effective cooperation with regulatory authorities.

Who is winning the race to net zero?

Most financial services companies have set their net-zero targets for 2050. GlobalData has analyzed the targets, emissions data, and net zero strategies of 20 leading financial services companies. All companies have set classified net zero targets covering Scope 3 emissions. No companies currently have SBTi-verified net-zero targets.

The leading companies based on GlobalData’s ranking are shown below. Performance is judged on a company’s emissions reduction targets, the types of decarbonization strategies adopted, its progress in the pursuit of net zero, and the quality of its emissions reporting according to international standards.

Understanding emissions across the financial services value chain

Financial services companies should focus on reducing Scope 2 emissions. Scope 2 reporting is mostly centered on purchased electricity. This can be market-based, which is based on the emissions generated by individual electricity suppliers, or location-based, which is based on the emissions intensity of the local power grid.

Scope 2 emissions are usually the easiest to reduce, as to do so, a company only needs to buy fully renewable electricity from an electricity supplier. This will reduce market-based Scope 2 emissions, but not location-based Scope 2 emissions.

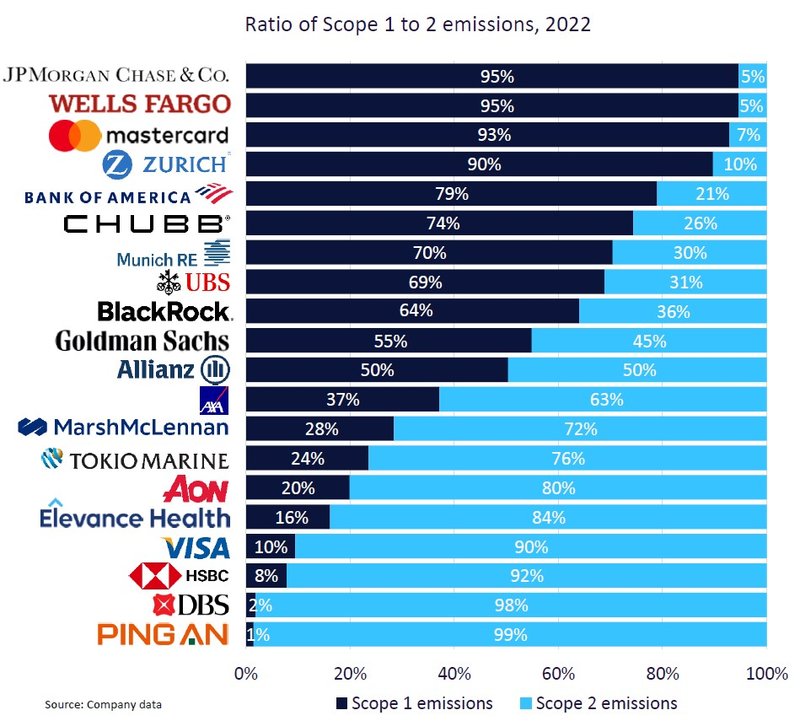

Scope 1 emissions are comparatively lower for financial services companies compared to other sectors. This is because very few of their assets directly emit GHGs.

The largest source of emissions in the financial services sector is Scope 3 emissions. For most of the 20 finance majors analyzed by GlobalData, business travel was the only sub-category of Scope 3 emissions that was reported.

The largest components of Scope 3 emissions will eventually be financed emissions. These are not yet comprehensively reported. Over the last two years, major banks have begun disclosing financed emissions intensity and reduction targets for high-emitting sectors.

For payments companies, the largest proportion of their emissions comes from purchased goods and services. As such, a large part of their net-zero strategies involves engaging with their suppliers, encouraging them to disclose emissions through the CDP (a carbon disclosure non-profit) and set emissions targets.

Emissions reduction strategies for the financial services sector

In Scope 1 and 2 emissions, financial services companies are focused on reducing the carbon footprint of offices and data centers. They also seek to obtain certifications from environmental building standard organizations like LEED, BREEAM, Greenstar, WELL, Green Mark, and Fitwel.

Buildings:

- Strategies to reduce the emissions of corporate offices include using renewable energy, managing water usage and waste, and retrofitting LED lights.

- Some finance majors annually report the percentage of buildings that have achieved environmental certifications.

- Where office space is leased, green renovations are often undertaken on a case-by-case basis.

- Corporate office emissions naturally decreased from 2020–2022 as employees gradually transitioned towards remote working. However, financial services companies pushed for employees to return to offices to promote a work culture. In January 2023, Bank of America sent warning letters to employees threatening disciplinary action if they failed to comply with its new return to the office policy.

Data centres:

- Financial services companies hold a plethora of client information at data centers, so efforts to reduce their environmental impact are crucial for reducing Scope 1 and 2 emissions.

- Many payment companies saw their data center traffic spike during 2021 and 2022 in line with increased consumer spending across the broader economy.

- A key focus here is upgrading the cooling infrastructure to optimize airflow and improve water efficiency.

- Data center efficiency is typically measured using Power Usage Effectiveness (PUE), which divides the total amount of power entering a data center by the power used to run the IT equipment within it.

For the reduction of Scope 3 emissions, engaging with suppliers is essential. Supplier engagement is not just an emissions reduction strategy but is also a strategy to measure and report Scope 3 emissions more accurately.

Suppliers often represent a large portion of GHG emissions. Mastercard’s suppliers account for more than 80% of its emissions, with 50 accounting for more than 50% of this. Sometimes, supply chain emissions are concentrated in specific business units. For example, around 20% of HSBC’s 2022 supplier emissions stemmed from its real estate business.

For some financial services companies, their suppliers will also be their clients, creating natural opportunities for collaboration through environmental consulting services. CDP’s Supply Chain program helps companies engage more meaningfully with suppliers through annual surveys to better understand their emissions profiles.

Reducing financed emissions

Financed emissions (sometimes known as portfolio emissions) are GHG emissions linked to financial services companies’ investment and lending activities. The purpose of measuring and reporting financed emissions is for financial services companies to understand, assess, and take accountability for a portion of the environmental impact of their investment and lending portfolios.

In 2019, banks, investors, and fund managers worldwide partnered to publish the PCAF (Partnership for Carbon Accounting Financials) reporting standard. The standard stipulates that financed emissions should be calculated as a financial services company’s invested proportion of a client’s value multiplied by that client's absolute emissions. The PCAF standard is now the most widely adopted in the industry.

While reporting on financed emissions is currently not mandatory, pressure is mounting on financial services companies to recognize the role that their capital plays in facilitating climate change.

The PCAF recommends that financial services companies report on four metrics:

- Absolute emissions: The total GHG emissions of an asset class or portfolio. Used to set a baseline for emissions reduction.

- Economic emissions intensity: Absolute emissions divided by the loan or investment volume in EUR or USD, expressed as tCO2e/M(EUR) or tCO2e/$M loaned invested.

- Physical emission intensity: Absolute emissions divided by a value of physical activity or output, expressed as, e.g., tCO2e/MWh, tCO2e/tonne of product produced.

- Weighted average carbon intensity (WACI): A portfolio’s exposure to emission-intensive companies, expressed as tCO2e/M(EUR) or $M company revenue.

The PCAF has published methodologies to measure financed emissions across individual assets (equities, bonds, loans, project finance, real estate, mortgages, motor vehicle loans, and sovereign debt) and sectors. In addition to reporting absolute emissions, the PCAF recommends that financial services companies report on three intensity metrics to normalize data, making it more comparable across companies. Where provided, reporting on financed and insurance-associated emissions mostly focuses on the intensity of economic and physical emissions.

Climate related products: beware of greenwashing

Financial companies are incorporating sustainability into their range of products and services. Green bonds, for instance, have become a staple of sustainable finance.

Many financial services companies play an active role in developing global standards for green bonds. Allianz, Bank of America, and HSBC currently serve on the executive committee of the ICMA, influencing the management and administration of its Green Bond Principles (GBP). In addition, representatives of JPMorgan were among the co-authors of the GBP.

Following ICMA guidelines, most companies that issue green bonds also issue green bond frameworks that outline the projects they plan to invest in. Financial services companies tend to invest in renewable energy, energy efficiency, clean transportation, and green buildings. Mastercard, for example, allocated 80.4% of its total green bond proceeds between January 1, 2018, and December 31, 2022, to green buildings. Other categories include pollution prevention, biodiversity conservation, water and waste management, and circular economy-adapted products.

Financial services also play an important role in underwriting green bonds for non-financial corporations, with most major banks setting targets for how much sustainable finance they will underwrite.

However, companies should be aware of the greenwashing risks associated with climate-related products. Greenwashing is when companies exaggerate their sustainability to appeal to and win over consumers. Numerous regulatory initiatives have been implemented to combat greenwashing in financial products:

- The EU’s Sustainable Financial Disclosure Regulation (SFDR) requires asset managers to provide standardized disclosures on how ESG factors have been integrated at both an entity and product level.

- Similarly, the UK’s Sustainability Disclosure Requirements (SDR) is a set of anti-greenwashing rules to ensure that all sustainability-related financial product claims are fair, clear, and not misleading.

- In the US, the SEC enforces a set of ESG-related disclosure rules to promote transparency around ESG strategies in fund prospectuses, annual reports, and adviser brochures.

As a result, many financial services companies such as Goldman Sachs, Deutsche Bank, and BNY Mellon have faced investigations and fines over greenwashing allegations across 2022 and 2023. Funds that label themselves as ESG-oriented will continue to face scrutiny from regulatory authorities. Over time, this will lead to a higher quality market for sustainable funds.

For more insights into the path to net zero for companies, buy GlobalData’s report Net zero strategies in financial services.

GlobalData, the leading provider of industry intelligence, provided the underlying data, research, and analysis used to produce this article.

GlobalData’s Thematic Intelligence uses proprietary data, research, and analysis to provide a forward-looking perspective on the key themes that will shape the future of the world’s largest industries and the organisations within them.